Equity is the legal term for the amount of money you have in your property, being the value of the property less the balance of any mortgages. Transfer of Equity is therefore a change in the ownership of a property. This could be by adding another person, removing a person or transferring the property into the name(s) of new individuals. This will be done through altering the title deeds.

Despite what the name suggests, transfer of equity can be achieved without money changing hands. This is more common when parents wish to transfer the property into the names of their adult children for example, often for tax planning purposes.

It is common for people to transfer equity when they are going through changes in their family circumstances, including when a couple move in together, marry or form a civil partnership, or where a couple divorce/separate. Within divorce proceedings, a transfer of equity can be ordered by the court, or it can be by agreement between parties as part of a divorce settlement or separation agreement.

A transfer of equity is usually a straightforward transaction, providing there is no current mortgage on the property in question. The process will usually be quick (depending on individual situations) and will mainly involve submitting paperwork filled out by all parties to be submitted to the HM Land Registry.

Although it is still possible to transfer equity with a mortgage on the property, this does add some further stages to the transaction. Your mortgage lender will have to approve the transaction and will only do so if they are satisfied that it will not affect the monthly payments being made to them. This process is likely to cause the most delay in the transaction and therefore it is advisable to speak to your mortgage lender as soon as you have decided you wish to transfer equity.

Although we would recommend that all parties involved in a transfer of equity are represented by a solicitor, only the party buying out other parties must be legally represented. Seeking independent legal advice is always recommended when considering a transfer of equity.

A transfer of equity may also have some further implications surrounding Capital Gains Tax and Stamp Duty Land Tax. You can discuss your specific situation with your solicitor who will be able to advise you as to whether this applies to your transaction.

If you wish to find out some more information regarding a transfer of equity transaction, please contact our Client Service Advisors who will be able to assist you further.

A: There is no set rule as to which boundaries belong to a property. It is possible that your property is responsible for the left boundary, but it’s just as likely that all boundaries are yours.You can try to find out more via:

The transfer deed

The official title plan

The property information form

Check surrounding properties

Knowing which house boundaries to your property you own is something practical that people often don’t think about until any issues begin to arise.

A common misconception held by a lot of people is that you always own the boundary to the left of your property. Thinking about the practicalities of this leads to some questions; who owns the shared boundary to the rear? In a row of houses, surely someone must at some point own their right boundary in order for all boundaries to be maintained? What if the garden is an obscure shape with no defined ‘left’ boundary?

The truth is, there is no general rule as to which boundaries that a property owns. It is entirely possible that your property is only responsible for the maintenance of the left boundary but it is equally possible that you are responsible for maintaining all of the boundaries to the property.

It is likely that during the stress of a house move, your main concern is not which boundaries to the property you must maintain. In this respect, there are a number of ways in which you may be able to find out which boundaries to your property that you own.

The transfer deed (or previous transfer deeds for the property) may contain some details regarding which boundaries belong to the property. This is more likely if you are purchasing a new build property.

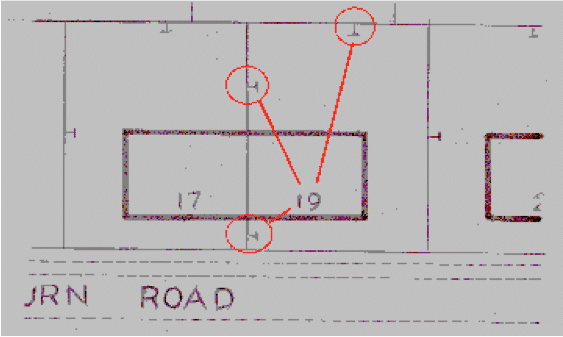

The official title plan for the property may show which boundaries are owned. This will be indicated by a ’T’ mark pointing inwards towards your property, as shown by the below diagram.

If not indicated in the transfer deed or official plan, it may be that you have to rely on the information provided by the seller in the Property Information Form. Of course, this will be less reliable than the official documents at points 1 and 2.

As a final resort, if no other information is provided in any of the above forms, it could be possible to infer which boundaries you own based on the surrounding properties on your street. This will never be a conclusive way of determining which boundaries are owned and should only be considered with the involvement of a conveyancer when all other options have been exhausted.

If you wish to find out anymore information regarding house boundaries or you need help with a boundary dispute, please contact our Client Service Advisors who will be able to assist you further.

Purchasing a new build property can be a daunting prospect if you are unfamiliar with the process. That’s why we have created a guide to help identify the steps you will take, as well as useful things to consider, to ensure that you successfully purchase your dream home.

Find the Developers building properties in your desired area – make sure that you thoroughly research and read any relevant reviews for these Developers. This will be particularly important if you are purchasing a property that is yet to be built or in an area that you are not familiar with.

Visit the New Build site or contact the Developer and find the home (or style of home) that you wish to buy.

Once Tinsdills has been instructed, we will issue you with a Client Care Pack which includes our Terms of Business, a request for proof of identity and payment on account for searches. You will need to sign and return the Terms of Business and provide the requested information to enable us to start work on your purchase.

You may have to pay a reservation fee to the Developers’ sales office in order to secure the property (this will usually only secure the property for 28 days). This reservation fee may not be refundable and you should consider the terms of any reservation agreement that you are asked to sign very carefully. The Developer will also perform their financial checks at this stage such as a credit check and ensuring that you have a mortgage offer in principle. At this stage you should consider whether you wish to use (and let the Developer know if so) the Help to Buy Equity Loan Scheme or the Shared Ownership Scheme, if applicable. Please see our article regarding the Help to Buy Loan here.

The Developer will send your solicitor the Reservation Form so that they can move forward with your purchase.

If you are having a mortgage, you should now apply to your chosen lender with the property details. (You will probably have a mortgage promise already at this point as this is necessary for most Reservation Forms). If you are using the Help to Buy Loan Scheme, they will need to authorise your mortgage offer.

Your mortgage lender should arrange a valuation survey for the property. If you are buying a property yet to be built, they will use the plans and specifications in order to do this.

The Developer will send your solicitor a Contract pack, together with all of the necessary information for the property. Your solicitor will raise any enquiries necessary at this stage.

Tinsdills will order the searches to be undertaken on the property. Searches are compulsory if you are having a mortgage. They are advisable on a cash purchase also, but not compulsory. Your solicitor will review the search results and again send any enquiries necessary to the Developer.

When you receive your formal mortgage offer, your solicitor should receive their copy at the same time. Your solicitor will draft the final completion statement and include details of any charges and payments required. These will include any additional payments that you have agreed with the Developer and the Developer will send your solicitor their financial Completion Statement. At this point your solicitor will advise the lender of any 3rd party payments’ (e.g. gifted deposit) and discuss with you if a co-ownership agreement is needed.

Once Tinsdills receive all search results, your mortgage offer and replies to any enquiries raised, your solicitor will prepare a Purchase Report for you.

Tinsdills will send you the Purchase Report, the Completion Statement, and any documents you may not have seen as yet. You will also be asked to make an appointment to see your solicitor to discuss the matter in detail, sign the documents required, discuss payment details for the deposit/balance due and finally, advise you of the completion date that the Developer expects to achieve. When exchanging Contracts on a New Build property, your solicitor will often do this with the Completion date ‘on notice’. This means that after exchange, your solicitor will wait to be informed that the property is ready in order to progress to legal Completion. There will usually be a timescale for this within the contract.

Once Tinsdills are in receipt of deposit funds from you, Contracts will be exchanged and your solicitor will send the deposit onto the Developer. As mentioned at stage 2, the property is usually held for 28 days with the reservation fee. This means that Contract exchange must happen before this period finishes in order to ensure the property is secured. This is something to consider if you need some time in order to access your funds etc. The Developer may well extend the period for which the property is held and Tinsdills can assist in negotiating this for you.

If your solicitor has exchanged contracts for completion ‘on notice’, when the property is physically complete, it will be inspected by the NHBC or other structural provider and your solicitor will be served with a notice providing a period of time, usually between 7-10 days to complete. You will be asked to complete your pre occupation inspection at this stage. It is very important that you inspect the property thoroughly; you will not be able to refuse to complete and/or retain any sums of money if the property is finished to your satisfaction at the end of the notice period.

Tinsdills will request the mortgage funds from your lender once there is a fixed Completion date – they usually require 5 working days notice. Any final balance due from you will also be requested at this time. If you are using the Help to Buy Loan Scheme, your solicitor will also request funds from them at this time. If you have a Help to Buy ISA, your solicitor will also request the relevant bonus.

Completion Day – Your solicitor will send the purchase price to the Developer by bank transfer. Once received by them, they will release the keys and you will be informed at that time by telephone. They will also provide you with any relevant paperwork for the site and any contents at this stage (or just after). This should include any guarantees and manuals.

After completion, your solicitor will arrange payment of your stamp duty (if required) and also apply to HM Land Registry to register the property in your name. Once this is finalised, you will receive a copy of your Title Information Document from your solicitor and your lender will also receive a copy. This process may take slightly longer for a newly built property as the property will not have been registered previously.

Things to Consider

Make a Snagging List Walk around your new home (if you are able) and identify anything that you don’t think has been completed to a satisfactory standard. These could include defects with fixtures and fittings or additional items that you paid for that have not been installed correctly, or even at all. The ideal time to make this list would be before Completion (and after Contract exchange if possible) but making sure you do this as soon as possible is advisable. These issues can then be fixed prior to Completion leaving less possibility of disputes about liability for the issues. A good way to avoid these issues would be to take a photo with a timestamp in order to show when the defect/issue was present.

Warranty With all New Build properties, the Developer provides a warranty; this may be an NHBC certificate, Architects certificate or some other guarantee. You should familiarise yourself with the limited scope of these guarantees.

Possibility for further development Consider whether any possible further development of the site after the current stage has been completed will affect your enjoyment of the property or its value. Speak to the Developer about any future plans they may have, a good indicator of this may be any land adjoining the development that is left undeveloped. This may not be something that you will receive an answer for, but is still something to consider.

Site Visit Visit the current and past sites for the Developer. This will give you an idea about the final property that you will be purchasing and its specifications, but will also give you a feel of the overall development. It will also allow you to see things such as access routes and new roads in person.

Leasehold v Freehold Consider whether you wish to purchase a freehold or leasehold property. If you are looking at a leasehold property, you will need to be aware of what is contained within the lease and any restrictions placed on the property. This is something that you will be made aware of within your Purchaser’s Report.

Long-Stop Dates Long-Stop dates are put in place by the Developer to set a final deadline for completion of the development of your property. If this deadline is not reached, you will be owed money by the Developer for the duration that the property is not completed beyond the deadline. Having a clear Long-Stop date in place with the Developer from the beginning ensures that you are aware of the timescales involved with your property allowing you to plan ahead and make any necessary arrangements. Always ask what the Long-Stop date affecting your property is.

Contact our team today for further advice and guidance on the purchase of a new build property.

During the process of buying a property, your solicitor will raise enquiries with the seller’s solicitor. This is a standard part of the buying process and is done to ensure that any potential issues are dealt with prior to Contract Exchange. Enquiries will usually be raised at two stages, dependent on the timeline of the transaction.

Once we have received the Contract, together with a copy of the deeds and the Property Information Form and Fittings and Contents Form from the seller’s solicitor, these will be checked and we will raise any enquiries necessary at this stage. These will be based on the documents received so far.

We will then order the searches to be undertaken on the property. Once we have received the results for these, we will review them and, again, send any enquiries necessary to the seller’s solicitors.

What happens after enquiries when buying a house?

Once we have received satisfactory responses to all enquiries raised, we will then progress your transaction towards Contract Exchange and Completion.

For more information about the property buying process, you can view our step by step guide to buying a property here.

If you would like some more information regarding our transparent costing for purchasing a home then please contact our Client Service Advisors for a quote.

If you are looking to purchase a new build property, you may be eligible for the Help to Buy Equity Loan Scheme run by the Government.

The scheme provides you with a loan of up to 20% of the cost of your newly built home (or up to 40% in London). You won’t be charged loan fees for the first five years of owning your home. After this, you will be charged interest at a rate of 1.75% for the first year and then this will increase each year in line with inflation.

Some conditions to being able to use the scheme are that:

You must not own any other property at the time of purchasing your new property using the Loan.

The property that you are purchasing must be worth £600,000 or less.

You must be able to provide a 5% deposit for the property.

Example

Let’s say you want to buy a new-build home worth £300,000. Using the Help to Buy scheme, you could put down a 5% deposit (£15,000), apply for an equity loan worth 20% (£60,000), meaning you would only need to get a 75% mortgage (£225,000).

Paying off your Loan

You must pay off your loan either after 25 years or when you sell your home. You will have to repay the Government 20% of the value of the property, even if the property has increased in value. For example if you purchased a property in 2015 for £200,000 and then sold the property in 2020 for £250,000, you will have to pay back the Government £50,000 when you initially borrowed only £40,000. This may be something to consider when deciding whether a Help to Buy Loan is appropriate for you.

You can also elect to pay back the loan early. If you can afford to do so before 5 years, then this will mean you avoid paying interest on the Loan.

Changes to Help to Buy Equity Loans from 1st April 2021

The scheme will only be available for first time buyers; those who haven’t previously owned or purchased property.

The scheme will introduce regional property price caps based on local markets. These will set the maximum price of a new build home that can be bought with Help to Buy in each region.

If you wish to take advantage of the current scheme then the purchase of your home must have reached legal completion by 31 March 2021.

It is also worth noting that the Help to Buy scheme will be coming to an end altogether on 31 March 2023.

Tinsdills Residential Property Team are highly experienced in both purchasing homes for clients using the scheme and assisting in redeeming the equity loan from Government. If you would like some more information regarding any of the above then please do not hesitate to contact the Team.

If you would like some more information regarding our transparent costing for purchasing a home using the Help to Buy scheme then please contact our Client Service Advisors for a quote.

Buying your first home can be a long and complicated process. We aim to be a helping hand for you throughout the first time buying process, from clarifying the procedure to carrying out actions that will lead to you turning the key to your very first home.

We’ve collated a handy timeline of the process to clarify every step that will lead you to owning your own home from Help to Buy ISAs to HM Land Registry.

The first step that most people take when looking to purchase a property is saving. If you’re using a Help to Buy ISA to save for your first home then the Government will boost your savings by 25%. This means that for every £200 you save the Government will give you £50 extra towards your savings.

The maximum Government bonus that you can receive is £3,000. Note that the deadline for opening a Help to Buy ISA has now closed so you’ll need a pre-existing account to receive this Government bonus.

Once you’ve considered how you’ll fund your deposit the process is usually as follows:

You’ll need to visit a mortgage advisor/lender to get a mortgage offer in principle.

Once your offer has been accepted on a property, contact Tinsdills to obtain a quote for conveyancing services.

Provide the estate agents with your Solicitor’s details.

Once the memorandum of sale has been produced by the estate agents your Solicitor will forward a ‘client care pack’ to you including their terms of business and outlining the next steps in the conveyancing process.

If you are having a mortgage a survey will be required which you will arrange with your mortgage provider. You can choose from a basic survey or something more in-depth like a Homebuyer’s Survey.

Following the results of your survey, if you are happy to proceed with the purchase, then you can complete and return the client care pack to your Solicitor. You will also need to produce your ID and make payment of money on account of searches.

The four standard searches that will usually be required for lending purposes will be a Local Authority Search, Environmental Search, Drainage Search and a Mining Search although this will depend on the location of the property.

If you are having a gifted deposit, details will need to be provided of the person gifting funds together with ID and proof of where the funds are coming from (e.g. bank account/savings passbook). Your Solicitor will explain their requirements to you.

Your mortgage lender will issue a formal mortgage offer to you when they have completed their checks. The mortgage lender will issue a separate copy of the mortgage offer together with details of their instructions in relation to your purchase to your Solicitor.

Your Solicitor will obtain and check the contract pack from the Seller’s Solicitor, request the appropriate searches and raise enquiries on the title.

Your Solicitor will then review the replies to the enquiries raised, review the search results and deal with any legal requirements on your mortgage offer and survey.

When your Solicitor has concluded their investigations they will report to you on the title and their findings in relation to the property. You will then be asked to make an appointment to come in to see your Solicitor to discuss your purchase in more detail and sign the necessary paperwork. At the meeting your Solicitor will discuss a completion date with you and once this date has been agreed with the Seller’s Solicitor your Solicitor will request the deposit from you.

If you are using a Help to Buy ISA your Solicitor will explain the bonus drawdown process to you and provide you with a declaration to sign confirming that you are a first time buyer. You will need to close your Help to Buy ISA account near to the completion date and provide your closing statement to your Solicitor.

Your Solicitor will use this declaration, together with the closing balance statement, to apply for your HTB bonus from the Government Help to Buy portal. The bonus money will be held on your client account until we are ready to complete your purchase.

You should note the bonus cannot be used as part of your deposit but can be used as the final contribution towards the purchase price on completion. Further details can be found at the following link; https://www.helptobuy.gov.uk/help-to-buy-isa/how-does-it-work/

When a completion date has been agreed your Solicitor will submit the Certificate of Title to your mortgage lender confirming that the legal requirements have been satisfied. Your Solicitor will request the mortgage advance to be released in readiness for completion. You will be asked to pay any balance funds due including your legal fees and Stamp Duty Land Tax (if applicable) prior to completion.

When all parties are ready Contracts are exchanged, your deposit is paid and the agreed completion date then becomes fixed. You will be asked to arrange buildings insurance for the property from the date of exchange of Contracts.

The mortgage advance will be sent from your mortgage lender to your Solicitor in readiness for completion.

Your Solicitor will undertake the pre-completion searches and completion will then take place on the arranged date. You will be informed when the keys are ready for you to collect from the estate agents.

On your behalf your Solicitor will then make payment of the Stamp Duty Land Tax (if applicable) to the Inland Revenue. Your Solicitor will then register you as the new owners of the property at H M Land Registry. This can take up to 6 months due to H M Land Registry timescales.

Once the registration is completed a copy of the updated title will be forwarded to you showing you as the registered owner of the property. You will have successfully purchased your first property.

Throughout the whole first time buying process you’ll have your dedicated team at Tinsdills on hand for clarification and assistance. Our aim is always to deliver clarity and confidence while you take life’s biggest steps. Feel free to contact us today by calling 01782 652300, or dropping us an email at lawyers@tinsdills.co.uk.

As of April 6th 2020, the pre-existing deadlines in place for paying Capital Gains Tax following the sale of a residential property are changing in the UK. To be as prepared as possible, you need to understand these changes.

From the aforementioned date, you will have approximately 30

days to inform HMRC and pay owed Capital Gains Tax – if you are a UK resident

selling a residential property in the country.

Should you fail to inform HMRC about your Capital Gains Tax

within the 30-day post-completion window, you could receive a penalty and be

made to pay interest on top of what you already owe. Because of these potential

consequences, it is crucial that people fully comprehend the changes.

What is Capital Gains Tax?

Put simply, Capital Gains Tax is what you pay on any profit

you make following the sale or disposal of an asset that’s value has increased.

In these situations -you need to report Capital Gains Tax within 30 days

If you sell or dispose of any of the following, you might

need to report on your Capital Gains Tax and make a payment:

A property that hasn’t been used as your home

A property used for holidays

A property that you let out for others

An inherited property that hasn’t been used as

your home

However, you will not be required to report or pay if:

A contract for sale was made prior to 6th April 2020

The Private Residence Relief criteria are met

The sale was to a spouse or civil partner

The profit gains fall within tax-free allowance

The property was sold at a loss

The property exists outside of the UK

Online Service to be Launched

HMRC are launching an online platform that lets you report on or pay any Capital Gains Tax owed by yourself.

Advice for Agents

Do you act as an agent for a person who is selling or

disposing of residential property in the UK? If so, you need to:

Register with Agent Service

Ensure that Capital Gains Tax owed by any of

your clients is reported and paid within the 30-day window following completion

If you’re a non-UK resident

Are you a non-UK resident? If so, you will need to carry on

reporting the sale/disposal of any UK property and/or land. You must do this

even if there is no Capital Gains Tax owed within the 30-day window following

completion.

You will no longer be allowed to defer any Capital Gains

payment you owe through a Self-Assessment return, and any you owe will have to

be paid within the 30-day window.

Included in this is the disposal of residential property,

non-residential and other disposals.

From April 6th 2020, non-UK residents can use the

new online platform, which is replacing the pre-existing reporting service.

If you are a non-UK resident, you can discover whether you

need to pay Capital Gains Tax here.

What About Trusts?

Do you represent a Trust? If so, you will need to register at the Trust Registration Service. For existing Trusts, you can utilise your UTR in order to gain access to the new service.

If you represent a Trust for a UK-based resident who

sells/disposes of UK residential property, you will need to make sure any

Capital Gains Tax owed is reported & paid within the 30-day window

following completion.

Similarly, if you represent a Trust for a non-UK resident

who sells/disposes of UK residential property, you will need to make sure any

Capital Gains Tax owed is reported & paid within the 30-day window

following completion.

[vc_row][vc_column][vc_column_text]Buying a leasehold can be a complex process, and having questions is perfectly normal. Luckily for you, we have compiled this comprehensive guide on all things leasehold. Here we answer, in detail, 12 key questions that people might have when entering into this process. If you get to the end of this piece and still have questions, we are just a short phonecall or email away. However, the chances are you’ll find exactly what you’re looking for right here…

How long is left on the lease?

During the process of buying a leasehold, you buy the right to possess the property for the remainder of the term of the lease. When drawn up in the past, leases have been anything between 99 years and 999 years. Obviously, as the years go by, the term reduces.

The law allows you to require that the landlord extends the lease once you have owned the property for two years, but the cost of that lease extension goes up dramatically once the term of the lease is less than 80 years. For this reason, some mortgage lenders want there to be as much as 90 years left to run so that you have time to extend the lease before the costs go up.

How much is the ground rent?

Ground rent is the amount that the lease says you have to pay to the landlord every year – for nothing. Yes, you do not get anything in return for ground rent other than to be able to say that you have complied with the requirements of the lease. If you fail to pay the ground rent then the law allows the landlord to take you to court, so you need to know that you can afford it and should always pay it if there is a dispute over the rent. You can claim it back later if you win the dispute.

Ground rent can be anything from a peppercorn (basically a nominal value so you do not actually pay anything) to many thousands of pounds, and it can go up further.

Is there a ground rent review clause?

You need to ask your property lawyer whether there is a rent review clause and how that operates. If there is a calculation, you should run the calculation for at least 50 years to see what the payment would look like. There have been some badly-worded rent review clauses that have resulted in ground rents in the region of millions of pounds.

How often is the rent reviewed?

Most lenders require that the rent is not reviewed more often than every 20 years, so you need to check that your lease will comply with that.

When is the next review?

It may say that rent is reviewed every 20 years, but you need to know from when. Some lease start dates are well before the actual date of the lease, because the builder might start all their leases on the same date within an estate. If you are buying a leasehold that is one of the last plots to be sold on the estate then the lease may already have been running for several years, so you may find that your rent is reviewed or your lease will become ‘short’ much sooner than you would think.

How much is the service charge?

Service charges are the contribution by the property owners towards the maintenance of the shared areas and amenities. These vary hugely depending on how big the communal areas are and the type of shared amenities. You can imagine that if you have access to a marina or leisure facilities then these can be very high, whereas if you have a leasehold house which only has to contribute towards a small space of communal garden – then hopefully the service charge would be pretty low.

Are there any major expenditures coming up?

Where there are major expenditures, the landlord has to consult with leaseholders before committing to having the work done. Your property lawyer will ask if there are any Section 20 notices revealed which would indicate if works were planned. However, you need to ask your surveyor to see if they can foresee any work that might come up which has not yet been consulted on.

Is there a sinking or a reserve fund?

Every leasehold estate should have an asset management plan detailing what the likely costs will be to maintain the properties in the estate. This should result in an additional payment to the service charge, which goes into the reserve fund to build up funds, so that when a large expenditure does come up you don’t have to find thousands of pounds. Once paid into the reserve fund you won’t get the money back but similarly, when you buy the property you will get the benefit of the monies already accrued in the reserve fund.

What consents do I need?

The lease may well contain additional requirements for you to obtain the consent of the landlord. For example, if you want to alter, extend or let the property, but also if you want to keep a pet or run a business from the property. Therefore, you need to know whether you have to get consent and, if it is going to be important to you, make obtaining consent a condition of your purchase of the property.

What are the administrator’s fees?

When buying a leasehold the lease administrator will charge fees for administering the lease. The lease administrator might be a landlord, a management company, a managing agent, a right to manage company, a housing association, a residents’ association or a legal representative of any of the above.

There could also be more than one lease administrator all of whom may want to make a charge for the administration of the lease.

Ask your property lawyer to ask the lease administrator for a menu of their charges so that you know how much it will cost you if you want to sell, let, re-mortgage, extend or do anything that requires their consent within the lease. The administration fees can be very high, and you generally have no right to challenge how reasonable they are through the courts.

Are event fees payable?

Some leases contain a requirement that if you sell, let or re-mortgage the property you have to pay a percentage of the value of the property at that time to the landlord. Sometimes event fees are created as a way to offset service charges during the ownership, particularly in retirement homes, but in other cases it is just an additional payment to the landlord.

Is the lease acceptable to mortgage lenders?

Whether or not you are buying a leasehold with a mortgage you need to know that you will be able to sell on the open market or take a mortgage out in the future if you need to. It is therefore incredibly important that you know whether the lease is acceptable to mortgage lenders. Of course, a lending policy does change so do beware that just because it is okay now does not mean it will be acceptable in the future.

For example, some lenders have changed their policy so that they will not lend on leases which have ground rents of more than £250 (£1,000 in Greater London). This is because they can be caught by the provisions of the Housing Act 1988, which would turn the lease into an assured shorthold tenancy that would give additional rights to the landlord if you fall behind on payment of the ground rent. The Government have committed to change this law, but until it does you need to make sure that your lease meets the lender’s policy.

There are lots of other complications to leasehold, so make sure that you read your property lawyer’s advice thoroughly and question anything which you do not understand or which conflicts with what you have been told already.

There are lots of leases out there which are absolutely fine – you just need to make sure that you are buying one of them. It is worth noting that the majority of these 12 questions require information which the person marketing the property should have available under the Consumer Protection from Unfair Trading Regulations 2008. Be sure to ask them for their material facts disclosure for the property.

If you require further advice on buying a leasehold and other related issues, feel free to get in touch with us by giving us a call on 01782 652300, or sending an email to lawyers@tinsdills.co.uk.[/vc_column_text][/vc_column][/vc_row]

A recent article from the BBC claims that new home freeholds aren’t “worth the paper they’re written on”, with one person saying “I don’t trust landlords and leaseholds. I promised myself I would never get involved with a leasehold property. Now finding out my freehold isn’t worth the paper it’s written on makes me so angry.”

Andrew Burrows – Director and Head of our Residential Property team says “it’s very important when buying a property that you get the correct advice, and this can be particularly important when buying a new build property.”

The article also states “once the estate is finished and handed over to a management company, Denise (resident) will be charged each year for services such as the upkeep of the green spaces and the maintenance of the roads. However, she doesn’t have any control over what that rent charge might increase to in the future.”

Following on from this, Andrew suggests the way that planning permission is currently granted for developments means that developers will be forced to create a green or open space in the development. Whilst this will provide a significant amenity for the residents, once the development is completed the builder will want to hand over responsibility for its maintenance to the residents. This is usually achieved by the residents being forced, upon purchase of the property, to become involved in a management company ran by the residents themselves. In some cases, residents can even be forced to become officers of the company.

The maintenance of these open spaces, and the fees associated with the running of the company such as accountants fees, are levied on residents as an annual payment, usually called a rent charge. The exact amount for this isn’t fixed in the deeds, and so can rise unexpectedly. This can lead to complex legal arguments regarding sanctions for the non-payment of these charges, which can delay or even prevent a property being sold.

Proposals are being made to regulate these charges more closely, but given the present political climate, it is difficult to guess when these may become law.

The BBC also proposes “Covenants are intended to preserve the amenity and outlook of the wider estate and to promote good neighbourly relations and when planning the estate, the developer will need to form a view as to how restrictive the covenants should be.”

Andrew backs this up by suggesting, sometimes to reflect planning conditions but sometimes for the developers benefit, the deeds will contain restrictions called Restrictive Covenants. These can prevent alterations to the property, parking certain types of vehicles, or preventing running a business. It’s important that these are considered before committing to the purchase, as they may hinder your plans for the property and not be acceptable to future buyers.

Whilst it’s not always easy, the best approach is to look past the glossy sales brochures and the pristine show homes to truly consider, with an independent and suitably qualified and experienced lawyer, exactly what you are signing up to.

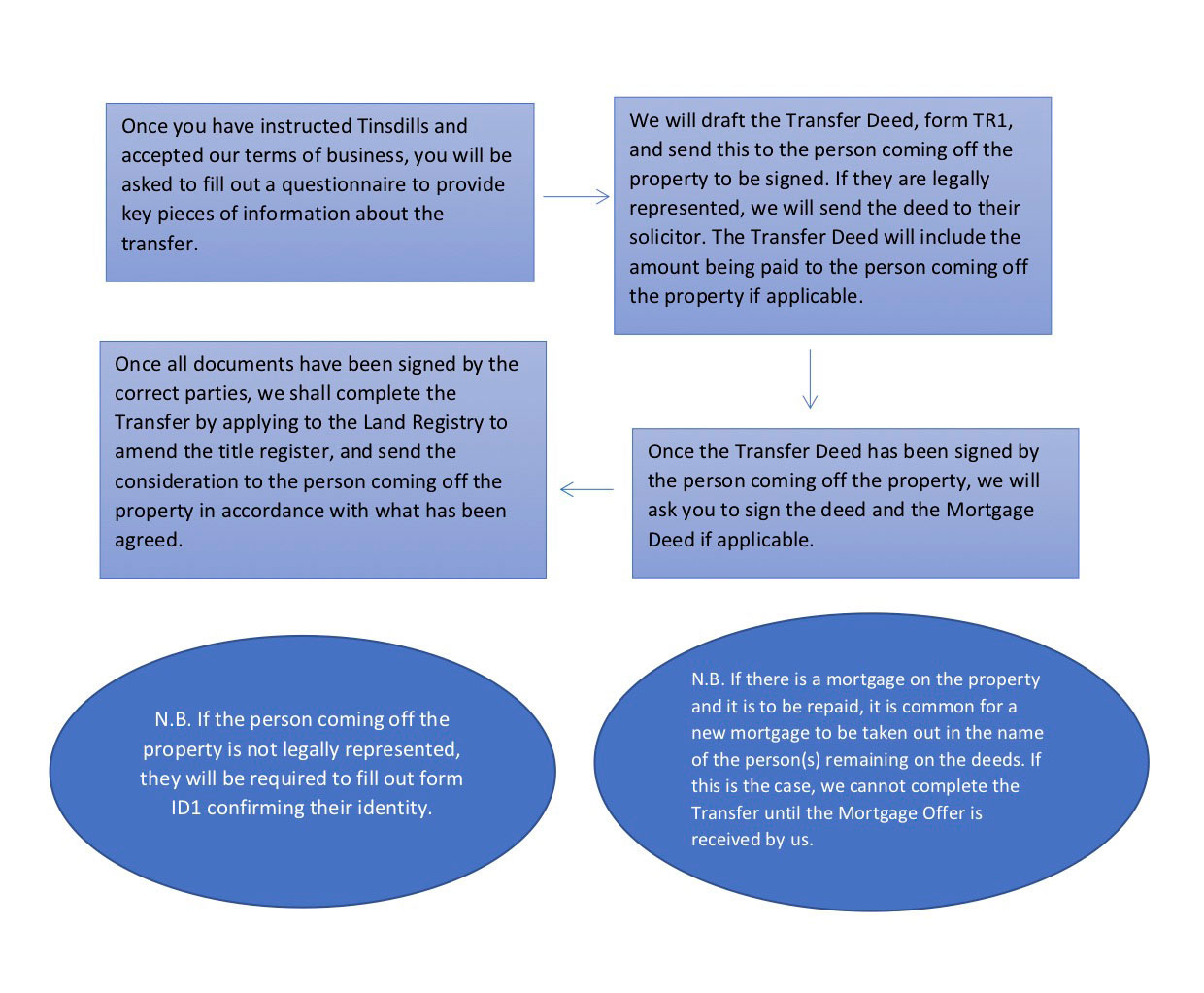

[vc_row][vc_column][vc_raw_html css=”.vc_custom_1583256483862{background-color: #ffffff !important;}”]JTNDYm94JTNFJTIwJTNDcCUzRSUyMCUzQ2IlM0UlMjBIb3clMjBkbyUyMEklMjByZW1vdmUlMjBhJTIwbmFtZSUyMGZyb20lMjBhJTIwdGl0bGUlMjBkZWVkJTNGJTIwJTNDJTJGcCUzRSUyMCUzQyUyRmIlM0UlMEElM0NwJTNFJTBBMS4lMjBGaWxsJTIwaW4lMjBhJTIwcXVlc3Rpb25uYWlyZSUyMHRvJTIwcHJvdmlkZSUyMGtleSUyMGluZm9ybWF0aW9uJTIwcmVnYXJkaW5nJTIwdGhlJTIwdHJhbnNmZXIuJTBBJTNDJTJGcCUzRSUyMCUzQ3AlM0UlMEEyLiUyMFdlJTIwd2lsbCUyMGRyYWZ0JTIwdGhlJTIwdHJhbnNmZXIlMjBkZWVkJTIwJTI4VFIxJTI5JTIwYW5kJTIwc2VuZCUyMHRoaXMlMjB0byUyMHRoZSUyMHBlcnNvbiUyMGJlaW5nJTIwcmVtb3ZlZCUyMGZvciUyMHNpZ25pbmcuJTBBJTNDJTJGcCUzRSUyMCUzQ3AlM0UlMEEzLiUyMFdlJTIwYXBwbHklMjB0byUyMHRoZSUyMGxhbmQlMjByZWdpc3RyeSUyMHRvJTIwYW1lbmQlMjB0aGUlMjB0aXRsZSUyMHJlZ2lzdGVyJTJDJTIwYW5kJTIwc2VuZCUyMGNvbnNpZGVyYXRpb24lMjB0byUyMHRoZSUyMHJlbW92ZWQlMjBwYXJ0eS4lMEElM0MlMkZwJTNFJTIwJTNDcCUzRSUwQTQuJTIwWW91JTIwd2lsbCUyMHNpZ24lMjB0aGUlMjBkZWVkJTIwJTI4JTI2JTIwbW9ydGdhZ2UlMjBkZWVkJTIwaWYlMjBuZWNlc3NhcnklMjkuJTIwQWxsJTIwZG9uZSUyMSUyMCUzQyUyRnAlM0UlMjAlM0MlMkZib3glM0U=[/vc_raw_html][vc_separator][vc_column_text]There are several reasons why you might need to know how to remove a name from a title deed for a property, and each situation calls for various courses of action, which are listed below.

Here we will detail the process of removing a name from a title deed in the most straightforward circumstances, before detailing amendments in accordance with common complications.

The process of removing a name from a title deed is called a transfer, of which there are three main types:

A gift of no consideration: This means that the previous owner signs over their share of their property with no expected benefits i.e. no money changes hands.

The removal of a name following death.

A transfer 2-1 with or without a mortgage: Where there is a mortgage or financial consideration involved, lender approval must be sought or a new mortgage put in place in the name of whichever party is retaining the property.

The Steps – Acting on behalf of the person remaining on the title deed (2-1 Transfer)

Other Considerations

There are a few things that you’ll need to consider when attempting to remove a name from a title deed. These are:

Matrimonial advice

The transfer doesn’t mean that the person being removed from the deeds to the house can’t claim on a divorce.

Insolvency advice

If the transfer is to avoid a property being given to creditors in the case of bankruptcy, this can be set aside by trustees in the bankruptcy.

Leasehold properties

You may need the Freeholder to consent to the transfer.

Short ownership

If the property has been owned less than 6 months and there will be a new mortgage on the property, your lender will need to approve this.

Stamp duty land tax

Stamp Duty may be payable under some circumstances.

If the transfer is a gift for no consideration, which can mean that the transfer works as a gift from parents to children, you’ll need to consider the following things:

Whether the transfer is consistent with wills/tax advice/financial advice.

Your rights to continuing occupation, and associated costs.

Any nursing home/care fees.

Similarly, if the transfer is the removal of a name following death, you’ll need to be aware of the following processes:

Property owned jointly

You will need to make an application at the Land Registry to remove the name. The application will need to be supported by a copy of the death certificate.

Property owned in common

You may need to appoint trustees and take out a grant of probate.

How We Can Help?

At Tinsdills Solicitors, we specialise in simplifying the process so that you can complete the transfer in full confidence, knowing that every box is ticked and you’re fully aware of what’s happening in every aspect of the journey.

If you require help regarding removing a name from a title deed, feel free to get in touch with us. You can give us a call on 01782 652300. Alternatively, you can drop us an email at lawyers@tinsdills.co.uk.[/vc_column_text][/vc_column][/vc_row][vc_row][vc_column][/vc_column][/vc_row]

Manage Consent

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.