Equity is the legal term for the amount of money you have in your property, being the value of the property less the balance of any mortgages. Transfer of Equity is therefore a change in the ownership of a property. This could be by adding another person, removing a person or transferring the property into the name(s) of new individuals. This will be done through altering the title deeds.

Despite what the name suggests, transfer of equity can be achieved without money changing hands. This is more common when parents wish to transfer the property into the names of their adult children for example, often for tax planning purposes.

It is common for people to transfer equity when they are going through changes in their family circumstances, including when a couple move in together, marry or form a civil partnership, or where a couple divorce/separate. Within divorce proceedings, a transfer of equity can be ordered by the court, or it can be by agreement between parties as part of a divorce settlement or separation agreement.

A transfer of equity is usually a straightforward transaction, providing there is no current mortgage on the property in question. The process will usually be quick (depending on individual situations) and will mainly involve submitting paperwork filled out by all parties to be submitted to the HM Land Registry.

Although it is still possible to transfer equity with a mortgage on the property, this does add some further stages to the transaction. Your mortgage lender will have to approve the transaction and will only do so if they are satisfied that it will not affect the monthly payments being made to them. This process is likely to cause the most delay in the transaction and therefore it is advisable to speak to your mortgage lender as soon as you have decided you wish to transfer equity.

Although we would recommend that all parties involved in a transfer of equity are represented by a solicitor, only the party buying out other parties must be legally represented. Seeking independent legal advice is always recommended when considering a transfer of equity.

A transfer of equity may also have some further implications surrounding Capital Gains Tax and Stamp Duty Land Tax. You can discuss your specific situation with your solicitor who will be able to advise you as to whether this applies to your transaction.

If you wish to find out some more information regarding a transfer of equity transaction, please contact our Client Service Advisors who will be able to assist you further.

Losing a loved one is a difficult and sensitive time for any family. It is hard enough to cope with bereavement without the added stress of having to deal with the inevitable paperwork that follows. When someone passes away, it is crucial that their estate is dealt with by the distribution of their assets and the settling of any debts, known as ‘estate administration’. At Tinsdills, we provide a sympathetic and efficient service to try to make the process of estate administration as stress-free as possible. That is why we have created the following guide to help walk you through what to expect.

Is there a Will in place? a) If the deceased left a Will, the first step is to locate the Will, check that it is valid and that it has been correctly executed (a valid Will names the Executors, who are responsible for administering the estate on behalf of your loved one). b) If the deceased did not leave a Will – i.e. a Will has not been created, the estate must be administered in accordance with the rules of intestacy. These rules are very rigid and govern who is entitled to administer the estate, known as the Administrators, and how the assets of the estate will be divided. c) The Executors or Administrators are known as the Personal Representatives of the estate.

Valuations a) A valuation of the estate’s assets and liabilities will now need to be obtained. This will include writing to investment companies, banks, building societies and estate agents etc. to determine the exact assets and liabilities of the estate at the date of death of your loved one.

Preparation of Documents a) Now that a valuation of the estate has been obtained, a HMRC Inheritance Tax return will need to be completed to report the value of your loved one’s estate to HMRC. The estate will either have Inheritance Tax to pay or it will be what is known as an ‘excepted estate’, where Inheritance Tax is not due. b) At the same time, the relevant application form needs to be completed, which brings together the information collected in relation to your loved one and the Personal Representatives of the estate, as well providing general details regarding the estate. c) The Inheritance Tax return and probate application form then need to be signed by the Personal Representatives. If there is a valid Will in place, the application to the probate registry will be for a Grant of Probate. If there is not a Will in place, the application to the probate registry will be for Letters of Administration.

Filing of Documents a) Once signed by the Personal Representatives, the Inheritance Tax return and application form need to be filed at the probate registry, along with the original Will, two copies of the original Will (if applicable) and your loved one’s death certificate. There will also be a fee due to the probate registry for them to process the application. b) If Inheritance Tax is due on the estate, the application form will generally be submitted once the Inheritance Tax has been paid or an arrangement has been agreed with HMRC regarding payment.

Issuing Grant of Probate or Letters of Administration a) Once the Grant of Probate or Letters of Administration has been granted by the probate registry, the Personal Representatives will have the formal authority to administer the estate.

Settling the Estate a) The Personal Representatives must now collect in the assets of the estate and pay any remaining debts or other expenses. b) All money from assets such as insurance policy claims, balance of bank and building society accounts and proceeds from the sale of shares or property should be collected in. c) When all assets have been collected in, any remaining debts of the estate should then be paid. d) The Personal Representatives should then prepare the estate account. This account should include a breakdown of the total assets, liabilities, fees and administration expenses of your loved one’s estate.

Distribution of the Estate a) Once all debts of the estate have been paid, the Personal Representatives should now distribute the estate in accordance with the terms of the Will or the rules of intestacy. b) Once the Personal Representatives can confirm that all monies have been accounted for within the estate, the estate administration is complete.

Tinsdills are highly experienced in estate administration matters and can deliver expert advice on your next steps. No matter what the circumstances, we will help you throughout this process.

If you would like to discuss estate administration matters in any further detail, please do not hesitate to contact Tinsdills’ highly experienced Wills, Trusts and Probate solicitors who will be pleased to assist you.

2020 has certainly been the year of change; many long-established business practices have had to be adapted in order to keep businesses and services going.

In a recent announcement it was revealed that the Government will introduce a temporary change in the law that allows Wills to be witnessed using video conferencing such as Facetime, Zoom and Skype during the coronavirus pandemic.

The temporary law is set to come in to force in September but will be back dated to include Wills executed from 31 January 2020 and the change is proposed to remain in place until 31 January 2022.

But is this too little too late, or is it something that will genuinely assist the most vulnerable during these unprecedented times?

This change in law has created a system that accommodates those who are shielding or unable to attend a Solicitor appointment, and gives clients peace of mind that they are able to create, amend or even execute their Will during these troubling times.

However, like any other new system, legal or otherwise, this change does not come about without practical implications that all legal practitioners should take into account. The legal requirements for creating a valid Will still rely heavily on the rules set out in the Wills Act 1837, which require the Will maker to sign their Will ‘in the presence of’ at least two independent witnesses. Only now, the new legislation allows for witnesses’ ‘presence’ to be physical or virtual, meaning that in order for a Will to be valid during a virtual Will signing certain criteria must be met:

The quality of the sound and video must be sufficient for the Will maker and witnesses to see and hear what is happening

The video-link must be in real-time, i.e. the witnesses cannot watch a pre-recorded video of the Will maker signing the Will

The witnesses must be able to see the Will maker actually sign the Will, so if for example the video only shows the Will maker’s head and shoulders, the Will cannot be valid

The witnesses must each sign the Will also via a video conference(s) (the guidance recommends that this should be done within 24 hours)

All signatures must be ‘wet’, remote electronic signatures will not be accepted

Ideally, best practice would advise that the meetings are also recorded, and the recordings kept for evidence.

Further implications then arise when considering how those who are self-isolating will actually get the Will to the witnesses. They would either need to go out to post the Will themselves or ask someone to collect it from them, in which case an arrangement to have the Will witnessed in person at a distance or through a window might well have been a simpler and arguably less risky solution in legal terms.

Additional consideration must also be given to circumstances where the Will is lost in transit or the Will maker dies before the witnesses have been able to sign it. Furthermore, there are arguments to suggest that the current requirements for witnessing Wills offer greater protection, making it harder for someone to be influenced to make a Will against their wishes; this protection may not necessarily be as robust during a video conference.

The Law Society argues that the Will reforms will “help alleviate the difficulties that some members of the public have encountered when making Wills during the pandemic”, but the society makes it clear that the government needs to ensure the legislation is drafted in a way that will “minimise unintended consequences and ensure validity.”

Making a Will is an important step and unfortunately the pandemic has created situations that mean the practicalities of having a properly executed Will can be both problematic and a matter of urgency. This new legislation will provide a temporary solution to those most at risk during the pandemic to ensure that their Wills can be executed properly and safely.

However, great caution should be taken if you are considering signing and witnessing a Will via video-conferencing before the legislation is published in September, and even then Wills should ideally be made in the physical presence of witnesses wherever possible to eliminate any room for doubt, leaving video witnessing as an absolute last resort.

During the process of buying a property, your solicitor will raise enquiries with the seller’s solicitor. This is a standard part of the buying process and is done to ensure that any potential issues are dealt with prior to Contract Exchange. Enquiries will usually be raised at two stages, dependent on the timeline of the transaction.

Once we have received the Contract, together with a copy of the deeds and the Property Information Form and Fittings and Contents Form from the seller’s solicitor, these will be checked and we will raise any enquiries necessary at this stage. These will be based on the documents received so far.

We will then order the searches to be undertaken on the property. Once we have received the results for these, we will review them and, again, send any enquiries necessary to the seller’s solicitors.

What happens after enquiries when buying a house?

Once we have received satisfactory responses to all enquiries raised, we will then progress your transaction towards Contract Exchange and Completion.

For more information about the property buying process, you can view our step by step guide to buying a property here.

If you would like some more information regarding our transparent costing for purchasing a home then please contact our Client Service Advisors for a quote.

If you are looking to purchase a new build property, you may be eligible for the Help to Buy Equity Loan Scheme run by the Government.

The scheme provides you with a loan of up to 20% of the cost of your newly built home (or up to 40% in London). You won’t be charged loan fees for the first five years of owning your home. After this, you will be charged interest at a rate of 1.75% for the first year and then this will increase each year in line with inflation.

Some conditions to being able to use the scheme are that:

You must not own any other property at the time of purchasing your new property using the Loan.

The property that you are purchasing must be worth £600,000 or less.

You must be able to provide a 5% deposit for the property.

Example

Let’s say you want to buy a new-build home worth £300,000. Using the Help to Buy scheme, you could put down a 5% deposit (£15,000), apply for an equity loan worth 20% (£60,000), meaning you would only need to get a 75% mortgage (£225,000).

Paying off your Loan

You must pay off your loan either after 25 years or when you sell your home. You will have to repay the Government 20% of the value of the property, even if the property has increased in value. For example if you purchased a property in 2015 for £200,000 and then sold the property in 2020 for £250,000, you will have to pay back the Government £50,000 when you initially borrowed only £40,000. This may be something to consider when deciding whether a Help to Buy Loan is appropriate for you.

You can also elect to pay back the loan early. If you can afford to do so before 5 years, then this will mean you avoid paying interest on the Loan.

Changes to Help to Buy Equity Loans from 1st April 2021

The scheme will only be available for first time buyers; those who haven’t previously owned or purchased property.

The scheme will introduce regional property price caps based on local markets. These will set the maximum price of a new build home that can be bought with Help to Buy in each region.

If you wish to take advantage of the current scheme then the purchase of your home must have reached legal completion by 31 March 2021.

It is also worth noting that the Help to Buy scheme will be coming to an end altogether on 31 March 2023.

Tinsdills Residential Property Team are highly experienced in both purchasing homes for clients using the scheme and assisting in redeeming the equity loan from Government. If you would like some more information regarding any of the above then please do not hesitate to contact the Team.

If you would like some more information regarding our transparent costing for purchasing a home using the Help to Buy scheme then please contact our Client Service Advisors for a quote.

Buying your first home can be a long and complicated process. We aim to be a helping hand for you throughout the first time buying process, from clarifying the procedure to carrying out actions that will lead to you turning the key to your very first home.

We’ve collated a handy timeline of the process to clarify every step that will lead you to owning your own home from Help to Buy ISAs to HM Land Registry.

The first step that most people take when looking to purchase a property is saving. If you’re using a Help to Buy ISA to save for your first home then the Government will boost your savings by 25%. This means that for every £200 you save the Government will give you £50 extra towards your savings.

The maximum Government bonus that you can receive is £3,000. Note that the deadline for opening a Help to Buy ISA has now closed so you’ll need a pre-existing account to receive this Government bonus.

Once you’ve considered how you’ll fund your deposit the process is usually as follows:

You’ll need to visit a mortgage advisor/lender to get a mortgage offer in principle.

Once your offer has been accepted on a property, contact Tinsdills to obtain a quote for conveyancing services.

Provide the estate agents with your Solicitor’s details.

Once the memorandum of sale has been produced by the estate agents your Solicitor will forward a ‘client care pack’ to you including their terms of business and outlining the next steps in the conveyancing process.

If you are having a mortgage a survey will be required which you will arrange with your mortgage provider. You can choose from a basic survey or something more in-depth like a Homebuyer’s Survey.

Following the results of your survey, if you are happy to proceed with the purchase, then you can complete and return the client care pack to your Solicitor. You will also need to produce your ID and make payment of money on account of searches.

The four standard searches that will usually be required for lending purposes will be a Local Authority Search, Environmental Search, Drainage Search and a Mining Search although this will depend on the location of the property.

If you are having a gifted deposit, details will need to be provided of the person gifting funds together with ID and proof of where the funds are coming from (e.g. bank account/savings passbook). Your Solicitor will explain their requirements to you.

Your mortgage lender will issue a formal mortgage offer to you when they have completed their checks. The mortgage lender will issue a separate copy of the mortgage offer together with details of their instructions in relation to your purchase to your Solicitor.

Your Solicitor will obtain and check the contract pack from the Seller’s Solicitor, request the appropriate searches and raise enquiries on the title.

Your Solicitor will then review the replies to the enquiries raised, review the search results and deal with any legal requirements on your mortgage offer and survey.

When your Solicitor has concluded their investigations they will report to you on the title and their findings in relation to the property. You will then be asked to make an appointment to come in to see your Solicitor to discuss your purchase in more detail and sign the necessary paperwork. At the meeting your Solicitor will discuss a completion date with you and once this date has been agreed with the Seller’s Solicitor your Solicitor will request the deposit from you.

If you are using a Help to Buy ISA your Solicitor will explain the bonus drawdown process to you and provide you with a declaration to sign confirming that you are a first time buyer. You will need to close your Help to Buy ISA account near to the completion date and provide your closing statement to your Solicitor.

Your Solicitor will use this declaration, together with the closing balance statement, to apply for your HTB bonus from the Government Help to Buy portal. The bonus money will be held on your client account until we are ready to complete your purchase.

You should note the bonus cannot be used as part of your deposit but can be used as the final contribution towards the purchase price on completion. Further details can be found at the following link; https://www.helptobuy.gov.uk/help-to-buy-isa/how-does-it-work/

When a completion date has been agreed your Solicitor will submit the Certificate of Title to your mortgage lender confirming that the legal requirements have been satisfied. Your Solicitor will request the mortgage advance to be released in readiness for completion. You will be asked to pay any balance funds due including your legal fees and Stamp Duty Land Tax (if applicable) prior to completion.

When all parties are ready Contracts are exchanged, your deposit is paid and the agreed completion date then becomes fixed. You will be asked to arrange buildings insurance for the property from the date of exchange of Contracts.

The mortgage advance will be sent from your mortgage lender to your Solicitor in readiness for completion.

Your Solicitor will undertake the pre-completion searches and completion will then take place on the arranged date. You will be informed when the keys are ready for you to collect from the estate agents.

On your behalf your Solicitor will then make payment of the Stamp Duty Land Tax (if applicable) to the Inland Revenue. Your Solicitor will then register you as the new owners of the property at H M Land Registry. This can take up to 6 months due to H M Land Registry timescales.

Once the registration is completed a copy of the updated title will be forwarded to you showing you as the registered owner of the property. You will have successfully purchased your first property.

Throughout the whole first time buying process you’ll have your dedicated team at Tinsdills on hand for clarification and assistance. Our aim is always to deliver clarity and confidence while you take life’s biggest steps. Feel free to contact us today by calling 01782 652300, or dropping us an email at lawyers@tinsdills.co.uk.

As of April 6th 2020, the pre-existing deadlines in place for paying Capital Gains Tax following the sale of a residential property are changing in the UK. To be as prepared as possible, you need to understand these changes.

From the aforementioned date, you will have approximately 30

days to inform HMRC and pay owed Capital Gains Tax – if you are a UK resident

selling a residential property in the country.

Should you fail to inform HMRC about your Capital Gains Tax

within the 30-day post-completion window, you could receive a penalty and be

made to pay interest on top of what you already owe. Because of these potential

consequences, it is crucial that people fully comprehend the changes.

What is Capital Gains Tax?

Put simply, Capital Gains Tax is what you pay on any profit

you make following the sale or disposal of an asset that’s value has increased.

In these situations -you need to report Capital Gains Tax within 30 days

If you sell or dispose of any of the following, you might

need to report on your Capital Gains Tax and make a payment:

A property that hasn’t been used as your home

A property used for holidays

A property that you let out for others

An inherited property that hasn’t been used as

your home

However, you will not be required to report or pay if:

A contract for sale was made prior to 6th April 2020

The Private Residence Relief criteria are met

The sale was to a spouse or civil partner

The profit gains fall within tax-free allowance

The property was sold at a loss

The property exists outside of the UK

Online Service to be Launched

HMRC are launching an online platform that lets you report on or pay any Capital Gains Tax owed by yourself.

Advice for Agents

Do you act as an agent for a person who is selling or

disposing of residential property in the UK? If so, you need to:

Register with Agent Service

Ensure that Capital Gains Tax owed by any of

your clients is reported and paid within the 30-day window following completion

If you’re a non-UK resident

Are you a non-UK resident? If so, you will need to carry on

reporting the sale/disposal of any UK property and/or land. You must do this

even if there is no Capital Gains Tax owed within the 30-day window following

completion.

You will no longer be allowed to defer any Capital Gains

payment you owe through a Self-Assessment return, and any you owe will have to

be paid within the 30-day window.

Included in this is the disposal of residential property,

non-residential and other disposals.

From April 6th 2020, non-UK residents can use the

new online platform, which is replacing the pre-existing reporting service.

If you are a non-UK resident, you can discover whether you

need to pay Capital Gains Tax here.

What About Trusts?

Do you represent a Trust? If so, you will need to register at the Trust Registration Service. For existing Trusts, you can utilise your UTR in order to gain access to the new service.

If you represent a Trust for a UK-based resident who

sells/disposes of UK residential property, you will need to make sure any

Capital Gains Tax owed is reported & paid within the 30-day window

following completion.

Similarly, if you represent a Trust for a non-UK resident

who sells/disposes of UK residential property, you will need to make sure any

Capital Gains Tax owed is reported & paid within the 30-day window

following completion.

Let’s face it, there are more cheerful things to think about than what happens to our assets when we die, and the thought of making a Will can seem quite a daunting process.

However, making a Will creates clarity and peace of mind both for you and those you leave behind, and with the right help the process can be simple and stress-free.

If you’re looking to write a Will, here are ten things that you should definitely consider:

1. What are your assets?

Before making your Will, you should take some time to consider and write down what the assets of your estate are, and their values. For example, this could include property, savings, investments, life policies and personal possessions. This exercise can be very helpful ahead of a meeting with your solicitor, as some financial or tax planning needs to be carried out as part of the Will making process. It will also help you to consider whether you want to make specific gifts or other arrangements relating to individual assets.

2. Who do you want to benefit under your Will?

This will depend upon your personal circumstances, but you need to consider whether any potential beneficiaries might need special consideration due to their age, vulnerability or other circumstances. It is also possible to grant rights over your assets for one beneficiary, but then have the asset pass to another beneficiary when those rights end. This can be particularly useful for property arrangements.

3. Who do you want to deal with your estate?

The Executors that you appoint in your Will are responsible for the administration of your estate and carrying out your wishes. You need to think carefully about who you appoint to this role as your executors need to be trustworthy and reliable, in order to guarantee that your wishes are properly carried out. If your estate is likely to be difficult or contentious, you may need to consider independent or professional executors. If you are leaving any part of your estate to someone who could be under 18 at the date of your death, or any other trust provision, you need to consider appointing at least two trustees to hold those assets in the terms of your Will.

4. Guardians

Although we all hope that it will never be necessary for Guardians appointed in our Will to act in said role, it is crucial to note that the decision of who to appoint is arguably the most important in writing your Will.

If you have children who could be under the age of 18 at the date of your death, then you should appoint guardians to look after them after your death until they reach the age of 18. The Guardians appointed under your Will take on parental responsibility for your children and therefore you need to consider this role and responsibility very carefully.

5. Inheritance tax

Once you have provided details of your assets, your solicitor will be able to advise you on whether there will be inheritance tax payable on your estate and if so, what you can do to reduce the tax bill.

6. Third-party threats

When you leave any part of your estate to a beneficiary, that inheritance then becomes part of the beneficiaries’ own estate for all purposes. This can leave the inheritance vulnerable to third-party threat, for example, from divorce, bankruptcy, poor decision-making, etc. If you are concerned about these third-party threats then it may be possible to safeguard part of your estate through the use of trusts.

7. Changes in circumstances

Are there any foreseeable changes to your circumstances that might alter the terms of making a Will? If so, you might need to build some flexibility into the Will, and trusts are often used to provide protection and flexibility.

Marriage and remarriage will automatically revoke (cancel) your Will unless it specifically states intentions to the contrary. A divorce won’t automatically revoke your will, but it can alter the terms of any will you have in place.

8. Proper signing and witnessing

Your Will isn’t valid until it is properly signed and witnessed. A Will that hasn’t been signed and witnessed correctly may be invalid or open to challenge.

9. Let people know

Once you have made your Will, and in particular if you have appointed someone to the role of Executor, Trustee or Guardian, then it would be sensible to let those people know that you have made a Will, where it is kept, and what role you have given them. It is also important that you keep your paperwork in good order so that your Will and estate assets can be easily identified after your death.

10. Review your Will

It is important that you review your Will periodically to ensure that it continues to reflect your current wishes. It is particularly important to review your Will if you (or any of your beneficiaries, Executor, Trustee or Guardian) have any significant change of circumstances. Even if the circumstances haven’t changed significantly, it is still worthwhile reviewing your Will periodically to keep up to date with changes in the law that might affect you.

The process of making a Will is much easier than you think. If you’re looking to create a Will, we recommend you contact us to have a chat about how we can make the process as simple and stress-free as possible for you. You can telephone us on 01782 652300 or email us at lawyers@tinsdills.co.uk right now.

[vc_row][vc_column][vc_column_text]We all hope to live out our days in relatively good health and independence. However, we also know that this isn’t guaranteed. If you become incapable of managing your own affairs due to ill health, you need to ensure that you have appointed somebody trustworthy to manage your affairs on your behalf. This Lasting Power of Attorney guide will help you towards doing exactly that.

It is always preferable that you decide who makes decisions for you in the event that you become incapable to make those decisions yourself later down the line. This is known as creating Lasting Powers of Attorney (LPA).

What is a Lasting Power of Attorney?

A Lasting Power of Attorney (LPA) is a document by which you can give another person or persons the authority to act/make decisions on your behalf if you are no longer able to do so.

What are the different types of LPA?

There are two types of LPA, one for property and financial affairs, and another for health and welfare. You can create an LPA for either one or both of these categories.

Property and Financial Matters: this type of LPA allows your Attorney(s) to deal with your financial affairs including decisions on:

Buying or selling property

Property management

Opening and closing bank accounts and investments

Receiving your income to use on your behalf

Paying your bills (including income tax)

Making investment decisions

Health and Welfare: this type of LPA allows your Attorney(s) to make decisions on your behalf about your health and welfare including:

Your day-to-day care, including diet and dress

Who you have contact with

Consenting to, or refusing, medical treatment

Assessments for the provision of care

Participation in social or leisure activities

How to make an LPA

Making an LPA is relatively straightforward, as each type of LPA is made using a specific form. The form itself is simple to fill out, but before you complete the form it is imperative that you have taken the time to carefully consider the following:

Who you wish to act as your Attorneys

Do you want to specify any guidance or instructions about how your Attorneys act for you?

If appointing more than one Attorney, how will decisions be made?

Do you wish to appoint replacement Attorneys in case one or more of your Attorneys can’t act for you?

People you wish to notify before your LPA is registered

Who will act as your Certificate Provider (an impartial person who is qualified to provide a certificate for the LPA)

Finally, once you have carefully considered the above, your LPA must be correctly signed and witnessed by all parties and then registered at the Office of the Public Guardian before your Attorneys can use it.

Who to appoint as Attorneys

An Attorney should be someone who is trustworthy, competent and reliable and they should have the skills to carry out the necessary tasks.

Attorneys can be appointed to act on their own, jointly with other Attorneys, or jointly and separately with other Attorneys (which means that they can act both independently or together). Attorneys can also be appointed jointly for some matters, as well as jointly and separately for others.

If you appoint more than one Attorney then you will need to think about their ability to work together, and also practical considerations like where the Attorneys live and how they are able to deal with the practical side of making decisions and managing your affairs.

If our Lasting Power of Attorney Guide has not answered all of your questions, feel free to give us a call on 01782 652300 or email lawyers@tinsdills.co.uk today.[/vc_column_text][/vc_column][/vc_row]

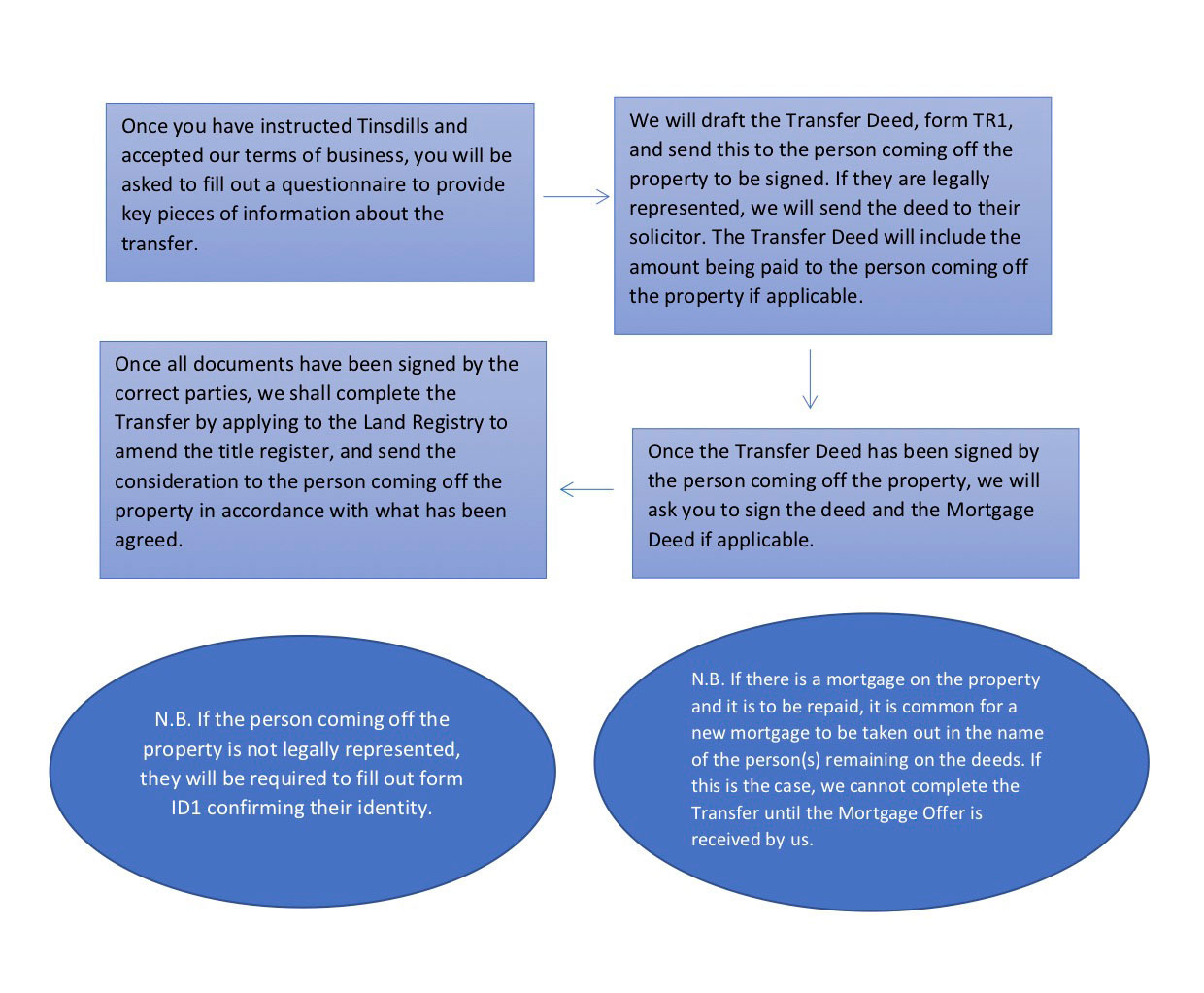

[vc_row][vc_column][vc_raw_html css=”.vc_custom_1583256483862{background-color: #ffffff !important;}”]JTNDYm94JTNFJTIwJTNDcCUzRSUyMCUzQ2IlM0UlMjBIb3clMjBkbyUyMEklMjByZW1vdmUlMjBhJTIwbmFtZSUyMGZyb20lMjBhJTIwdGl0bGUlMjBkZWVkJTNGJTIwJTNDJTJGcCUzRSUyMCUzQyUyRmIlM0UlMEElM0NwJTNFJTBBMS4lMjBGaWxsJTIwaW4lMjBhJTIwcXVlc3Rpb25uYWlyZSUyMHRvJTIwcHJvdmlkZSUyMGtleSUyMGluZm9ybWF0aW9uJTIwcmVnYXJkaW5nJTIwdGhlJTIwdHJhbnNmZXIuJTBBJTNDJTJGcCUzRSUyMCUzQ3AlM0UlMEEyLiUyMFdlJTIwd2lsbCUyMGRyYWZ0JTIwdGhlJTIwdHJhbnNmZXIlMjBkZWVkJTIwJTI4VFIxJTI5JTIwYW5kJTIwc2VuZCUyMHRoaXMlMjB0byUyMHRoZSUyMHBlcnNvbiUyMGJlaW5nJTIwcmVtb3ZlZCUyMGZvciUyMHNpZ25pbmcuJTBBJTNDJTJGcCUzRSUyMCUzQ3AlM0UlMEEzLiUyMFdlJTIwYXBwbHklMjB0byUyMHRoZSUyMGxhbmQlMjByZWdpc3RyeSUyMHRvJTIwYW1lbmQlMjB0aGUlMjB0aXRsZSUyMHJlZ2lzdGVyJTJDJTIwYW5kJTIwc2VuZCUyMGNvbnNpZGVyYXRpb24lMjB0byUyMHRoZSUyMHJlbW92ZWQlMjBwYXJ0eS4lMEElM0MlMkZwJTNFJTIwJTNDcCUzRSUwQTQuJTIwWW91JTIwd2lsbCUyMHNpZ24lMjB0aGUlMjBkZWVkJTIwJTI4JTI2JTIwbW9ydGdhZ2UlMjBkZWVkJTIwaWYlMjBuZWNlc3NhcnklMjkuJTIwQWxsJTIwZG9uZSUyMSUyMCUzQyUyRnAlM0UlMjAlM0MlMkZib3glM0U=[/vc_raw_html][vc_separator][vc_column_text]There are several reasons why you might need to know how to remove a name from a title deed for a property, and each situation calls for various courses of action, which are listed below.

Here we will detail the process of removing a name from a title deed in the most straightforward circumstances, before detailing amendments in accordance with common complications.

The process of removing a name from a title deed is called a transfer, of which there are three main types:

A gift of no consideration: This means that the previous owner signs over their share of their property with no expected benefits i.e. no money changes hands.

The removal of a name following death.

A transfer 2-1 with or without a mortgage: Where there is a mortgage or financial consideration involved, lender approval must be sought or a new mortgage put in place in the name of whichever party is retaining the property.

The Steps – Acting on behalf of the person remaining on the title deed (2-1 Transfer)

Other Considerations

There are a few things that you’ll need to consider when attempting to remove a name from a title deed. These are:

Matrimonial advice

The transfer doesn’t mean that the person being removed from the deeds to the house can’t claim on a divorce.

Insolvency advice

If the transfer is to avoid a property being given to creditors in the case of bankruptcy, this can be set aside by trustees in the bankruptcy.

Leasehold properties

You may need the Freeholder to consent to the transfer.

Short ownership

If the property has been owned less than 6 months and there will be a new mortgage on the property, your lender will need to approve this.

Stamp duty land tax

Stamp Duty may be payable under some circumstances.

If the transfer is a gift for no consideration, which can mean that the transfer works as a gift from parents to children, you’ll need to consider the following things:

Whether the transfer is consistent with wills/tax advice/financial advice.

Your rights to continuing occupation, and associated costs.

Any nursing home/care fees.

Similarly, if the transfer is the removal of a name following death, you’ll need to be aware of the following processes:

Property owned jointly

You will need to make an application at the Land Registry to remove the name. The application will need to be supported by a copy of the death certificate.

Property owned in common

You may need to appoint trustees and take out a grant of probate.

How We Can Help?

At Tinsdills Solicitors, we specialise in simplifying the process so that you can complete the transfer in full confidence, knowing that every box is ticked and you’re fully aware of what’s happening in every aspect of the journey.

If you require help regarding removing a name from a title deed, feel free to get in touch with us. You can give us a call on 01782 652300. Alternatively, you can drop us an email at lawyers@tinsdills.co.uk.[/vc_column_text][/vc_column][/vc_row][vc_row][vc_column][/vc_column][/vc_row]

Manage Consent

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.